Finance

Obligation Linéaire: A Full Guide to Understanding Belgian OLO Bonds

Introduction to Obligation Linéaire

Obligation linéaire, often called OLO, stands for a key type of Belgian government bond. These bonds help the Belgian government raise money for its needs. They come in euro and focus on medium, long, or very long terms. Each OLO forms part of a “line,” where all bonds in that line share the same interest rate and end date. This setup makes them easy to trade and combine. Investors like them for their safety since they back the full faith of the Belgian state. OLOs play a big role in Belgium’s debt system, making up most of its tradable debt. As of early 2026, the total value of OLOs in circulation sits around 468 billion euros, spread across 64 lines with end dates from 2026 to 2071.

Many people mix up obligation linéaire with other bonds, but it has unique traits. For example, they can be split into parts for interest and principal, known as stripping. This option adds flexibility for certain investors. Belgium started using OLOs in the 1990s to manage high debt levels, which have dropped over time. Today, they attract both big players and everyday savers looking for steady returns. Understanding obligation linéaire starts with seeing it as a safe way to lend money to a stable country like Belgium, with clear rules on how they work and trade.

History of Obligation Linéaire

Belgium introduced obligation linéaire in the early 1990s as part of efforts to handle its public debt. At that time, the country’s debt was high compared to its economy, reaching over 130% of GDP. The government needed a reliable way to borrow money, so it created OLOs as standard bonds that could be issued in batches. This approach allowed Belgium to build up debt lines over time, making it easier to attract investors. By the mid-2000s, there were about 22 lines, each worth around 10 billion euros, totaling roughly 220 billion euros. This was a big step from older methods, which were less organized.

Over the years, obligation linéaire evolved with market changes. In the 2010s, low interest rates led to new lines with lower coupons, some even at 0%. The Belgian Debt Agency took charge, improving issuance through auctions and syndications. Green OLOs appeared in 2018, focusing on eco-friendly projects. This shift showed Belgium’s push toward sustainable finance. By 2026, OLOs have grown to cover very long terms, like up to 2071, helping the government plan far ahead. The history shows how obligation linéaire adapted to economic ups and downs, from the euro crisis to recent inflation.

Key milestones include the first syndication in 1991 and the start of electronic trading. These changes boosted liquidity, meaning buyers and sellers could trade more easily. Debt reduction efforts in the 2000s cut the overall burden, but OLOs remained central. Today, they reflect Belgium’s solid credit rating, often AAA or close, drawing global funds. Learning this history helps see why obligation linéaire stays popular: it combines tradition with modern tools for steady borrowing.

Will You Check This Article: Understanding Onnilaina: A Complete Guide to Happy Loans

How Obligation Linéaire Works

Obligation linéaire functions as a loan from investors to the Belgian government. When you buy one, you give money now and get it back at maturity, plus interest along the way. Each OLO belongs to a specific line, with all in that line having the same coupon rate and due date. This uniformity makes them interchangeable, or fungible. Interest pays out yearly, based on the face value, usually 100 euros per unit. At the end, you get the full face value back. This simple setup appeals to those wanting predictable cash flows.

Issuance happens in tranches, meaning the government adds to existing lines over time. For instance, a line might start with 5 billion euros and grow to 20 billion as more are sold. This method keeps supply steady and avoids flooding the market. OLOs can have fixed or floating rates. Fixed means the interest stays the same, like 3% per year. Floating ties to benchmarks like EURIBOR. Most are fixed, offering certainty in uncertain times. Stripping allows splitting into zero-coupon bonds for principal and coupons, useful for matching specific needs.

Trading occurs on secondary markets, where you buy or sell before maturity. Prices fluctuate with interest rates: if rates rise, OLO prices fall, and vice versa. Yield measures the return, combining price and interest. For example, a bond at 95 euros with a 3% coupon might yield more than 3%. Obligation linéaire uses actual/actual for interest calculation, counting real days. This precision ensures fairness. Overall, the mechanics make OLOs a straightforward tool for government funding and investor savings.

Issuance Methods for Obligation Linéaire

The Belgian Debt Agency issues obligation linéaire mainly through auctions and syndications. Auctions happen monthly, based on a calendar set in December for the next year. In an auction, the agency picks lines to reopen and invites bids from primary dealers—big banks approved to deal directly. Bidders offer prices, like 101 euros per 100 face value, in multiples of 1 million euros, with at least 10 million per bid. The agency sets a cutoff price; higher bids win fully, while at-cutoff ones may get partial fills. Results come out quickly, and settlement is two days later.

Syndications suit new lines or large amounts. Here, a group of banks underwrites the issue, selling to their clients. This method ensures strong demand, often for benchmark sizes like 5-10 billion euros. For example, in January 2026, Belgium raised 8 billion via a 10-year OLO syndication at 3.4%. Primary dealers can also buy non-competitively after auctions, at average prices, up to certain limits. This rewards them for market-making. Optional reverse inquiries let dealers request specific OLOs, boosting liquidity. These methods keep issuance smooth and cost-effective.

Buybacks allow the agency to retire OLOs early, managing debt. In 2026, buybacks total over 2.5 billion euros across lines. Stripping withdraws capital for separate trading, with 10.8 billion stripped by early 2026, or 2.3% of outstanding. This adds options without new issues. Issuance focuses on euro, with no foreign currency OLOs. Green OLOs follow the same but fund green projects, like renewable energy. Understanding these methods shows how Belgium controls its debt supply to match investor appetite.

Maturity and Interest in Obligation Linéaire

Maturity in obligation linéaire ranges from 3 to 50+ years, covering medium (3-10 years), long (10-30), and very long (over 30). As of 2026, lines mature from March 2026 to June 2071. Shorter ones suit those wanting quick returns, while longer lock in rates for decades. For instance, the 2071 line has a 0.65% coupon, ideal for low-rate environments. Maturity affects risk: longer means more exposure to rate changes. The agency aims for even distribution to avoid big refunds at once.

Interest, or coupon, pays annually on the due date, like June 22 for many lines. Rates vary: older lines have high coupons, up to 5.5% for 2028 maturity, while recent ones are lower, like 0% for some 2027s. Average coupon across lines is around 2-3%. Yield to maturity factors in purchase price; buying below face value boosts yield. For a 3% coupon bond at 98 euros, yield exceeds 3%. Interest calculation uses actual days, so February 29 counts. This accuracy prevents disputes.

Floating rate OLOs, though rare, adjust with market rates, protecting against inflation. Most are fixed, providing stability. At maturity, the National Bank of Belgium pays principal and final interest. Early sale on secondary market gets market price, which could be gain or loss. Taxation applies: in Belgium, interest faces 30% withholding tax, but exemptions exist for some holders. Maturity and interest make obligation linéaire versatile for portfolios, from pensions to short-term holds.

Benefits of Investing in Obligation Linéaire

One main benefit of obligation linéaire is safety. Backed by Belgium’s government, they have low default risk. The country’s AA credit rating from agencies like S&P confirms this. Investors get steady income from coupons, perfect for retirees or funds needing reliable cash. Liquidity stands out: with 468 billion outstanding, trading is easy on platforms like MTS. Primary dealers ensure buy/sell quotes, reducing wait times. This makes OLOs better than less liquid assets.

Diversification is another plus. Adding obligation linéaire to a mix of stocks or other bonds lowers overall risk. They often move opposite to equities during downturns, acting as a buffer. For euro-zone investors, no currency risk exists. Green OLOs appeal to those wanting ethical investments, funding clean energy or transport. Yields, while not the highest, beat savings accounts; a 10-year OLO at 3.4% in 2026 offers decent returns post-inflation. Tax perks in some countries treat government bonds favorably.

For professionals, stripping adds value. You can separate coupons for targeted strategies, like matching liabilities. Fungibility means easy combining or splitting holdings. Compared to corporate bonds, lower yields come with higher security. Private investors access via banks, without needing auction participation. Overall, benefits make obligation linéaire a core holding for conservative strategies, blending income, safety, and ease.

Risks Associated with Obligation Linéaire

Interest rate risk tops the list for obligation linéaire. If rates rise, bond prices drop, leading to losses if sold early. For a 10-year OLO, a 1% rate hike could cut price by 8-10%. Long maturities amplify this; the 2071 line is very sensitive. Inflation risk erodes real returns: if prices rise faster than coupons, purchasing power falls. Low-coupon OLOs, like 0.1% for 2030, face this more.

Credit risk is low but present. Belgium’s debt-to-GDP around 100% in 2026 raises concerns if economy weakens. Downgrades could push yields up, hurting prices. Liquidity risk exists for stripped or off-run lines, though main ones trade well. Political risk from EU issues or Belgian divisions could affect. No default history helps, but vigilance matters. Currency risk hits non-euro holders if euro weakens.

Market risk ties to global events: pandemics or wars sway rates. Reinvestment risk occurs when coupons or maturity proceeds get lower rates upon rollover. Taxes can cut net returns; Belgium withholds 30% on interest for residents. Diversifying maturities mitigates some risks. While safe, obligation linéaire demands awareness of these factors for informed choices.

How to Buy Obligation Linéaire

Private investors buy obligation linéaire through banks or brokers, not directly in auctions. Open a securities account, then place an order for a specific OLO line by ISIN code, like BE0000350596 for a 2040 maturity. Banks charge fees, around 0.5-1% per trade. Check current prices on sites like Bloomberg or the Debt Agency’s reference list, updated daily around 3 PM. For new issues, subscribe during syndications via your bank if offered.

Professionals, like funds, use primary dealers for auctions. Become a recognized dealer to bid directly. Auctions require bids by noon on the day, with settlement two days later. Non-competitive buys follow for dealers. Secondary market trading happens on electronic platforms like MTS or over-the-counter. Use limit orders to set prices. For stripping, request through custodians like Euroclear.

Research first: look at yields, durations, and ratings. Tools like yield curves from the National Bank help compare. Minimum lots are often 1,000 euros, making it accessible. Track holdings in your account; interest credits automatically. Selling works similarly: place a sell order. Buying obligation linéaire needs KYC checks and tax info. Start small to learn, building a ladder of maturities for steady income.

Comparison of Obligation Linéaire with Other Government Bonds

Obligation linéaire shares traits with French OATs but differs in issuance. OATs use fungible tranches too, but France issues more volume, over 1 trillion euros vs. Belgium’s 468 billion. Yields are similar, with 10-year OATs at 2.5-3% in 2026, close to OLOs’ 3.4%. OLOs offer stripping widely, while OATs do too but with higher stripped portions (10% vs. 2-4% for OLOs). Both are euro-denominated, low-risk.

German Bunds are benchmarks, often with lower yields due to AAA rating. A 10-year Bund might yield 2%, less than OLOs’ 3.4%, reflecting Belgium’s AA status. Bunds lack green variants like OLOs. U.S. Treasuries differ in currency (USD) and size (trillions), with more liquidity. Treasuries pay semi-annually vs. OLOs’ annual. Inflation-linked options are rarer in OLOs.

UK Gilts match in safety but use GBP. Gilts have index-linked types protecting against inflation, an edge over standard OLOs. Maturity spreads are similar, up to 50 years. Overall, obligation linéaire suits euro-focused investors wanting Belgian exposure, with competitive yields and green options setting it apart.

Recent Developments in Obligation Linéaire

In 2026, Belgium launched a new 10-year obligation linéaire via syndication, raising 8 billion euros at 3.4% coupon, maturing in 2036. Demand hit records, showing investor confidence amid stable rates. The Debt Agency canceled a January auction for this syndication, following tradition for benchmark issues. Green OLOs grew, with a 2040 line at 0.4% seeing more uptake for sustainable funds.

Auction volumes stayed strong, with monthly sales of 1-3 billion euros per line. Buybacks focused on near-maturing lines, like 2026 ones, to smooth refunds. Stripping rose slightly, now 2.3% of outstanding. Holdership shifted: foreigners hold more, up from past years, per National Bank data. Yields edged up with ECB policy, 10-year at 3.39% average.

Future plans include more green issues and longer maturities. The 2026 calendar lists 11 auctions, plus ORIs for liquidity. These steps address rising debt needs while keeping costs low. Recent changes highlight obligation linéaire’s role in adaptive finance.

Conclusion on Obligation Linéaire

Obligation linéaire offers a solid path for safe investing in Belgian government debt. With clear rules, from issuance to trading, it suits various needs. Whether for income or portfolio balance, OLOs provide reliability. As Belgium manages its finances, these bonds remain key. Consider your goals and risks before jumping in. With ongoing updates, obligation linéaire stays relevant in today’s markets.

For a barrister, the courtroom is a place of precision, logic, and meticulous detail. Yet, many of the UK’s most brilliant legal minds find that the same level of mastery does not always translate to their own balance sheets. Being a self-employed barrister is, in essence, running a high-stakes boutique consultancy where you are the sole product, the service provider, and the administrative lead.

The financial life of the Bar is unlike almost any other profession. You face the “feast or famine” reality of irregular income, the frustration of delayed case payments from solicitors, and a VAT regime that can feel like a labyrinth. While your focus remains on winning the next case, the underlying pressure of tax compliance and cash-flow management can become a silent burden.

Whether you are a junior tenant just starting your practice or a seasoned Silk looking to optimize a substantial portfolio, understanding the financial architecture of your career is essential. This guide explores the core pillars of financial success for barristers, from managing “Payments on Account” to identifying the niche deductions that generalist accountants often miss.

1. Understanding the Financial Structure of Barristers

How Barristers Work Financially

The vast majority of barristers in England and Wales are self-employed sole traders. Unlike many of your peers in the legal sector where accountants for solicitors often deal with partnership structures or limited companies, barristers generally cannot incorporate their practice. You operate as an independent contractor, usually within a “Chambers” structure.

The Relationship with Chambers

Chambers are not your employer; they are a service provider. You pay “chambers rent” or a percentage of your earnings to cover the cost of the building, administrative staff, and, most importantly, the clerks.

The Clerks and Billing

Your clerks are your primary business managers. They negotiate your “Brief fees” (the fixed fee for a case) and your “Refreshers” (daily court fees). However, while clerks are experts at billing, they are not tax advisors. They focus on billing income, but the responsibility for managing that income, setting aside tax, handling VAT, and preparing for retirement rests entirely on your shoulders.

Why Barristers’ Finances are Unique

The “delayed payment” culture in the legal industry is perhaps the greatest challenge. It is not uncommon for a barrister to perform work in January and not receive payment until July or even the following year. This disconnect between effort and reward makes traditional budgeting nearly impossible without expert intervention.

2. How Self-Employed Barristers are Taxed in the UK

As a self-employed professional, you fall under the HMRC Self-Assessment regime. Your tax is not deducted at source; instead, you pay tax on the profits your practice makes after allowable expenses are deducted.

Income Tax and National Insurance

You are subject to the standard UK progressive tax bands:

- Basic Rate (20%)

- Higher Rate (40%)

- Additional Rate (45%)

In addition to Income Tax, you must pay National Insurance Contributions (NICs). Following recent legislative changes, Class 2 NICs have been effectively abolished for most, but Class 4 NICs remain a percentage of your profits that must be factored into your annual liabilities.

The Self-Assessment Cycle

The tax year runs from 6 April to 5 April. The deadline for filing your digital return and paying your remaining tax for the previous year is 31 January. Missing this deadline results in immediate penalties, but for barristers, the real danger isn’t just the penalty .It is the “shock” of the bill itself.

3. Payments on Account: The “Double Bill” Surprise

If there is one area where junior barristers get caught out, it is Payments on Account. If your tax bill is more than £1,000, HMRC assumes you will earn at least the same amount next year. They require you to pay half of your next year’s estimated tax in advance.

The Scenario

Imagine it is your first full year of practice. You owe £20,000 in tax. On 31 January, you must pay:

- The £20,000 for the year you just finished.

- An additional £10,000 as the first “Payment on Account” for the upcoming year.

Suddenly, a £20,000 liability becomes a £30,000 cash requirement. Without a dedicated tax reserve, this can cause a significant cash-flow crisis. Expert financial planning involves calculating these “look-ahead” liabilities months in advance so there are no surprises when January arrives.

4. VAT Rules for Barristers: Timing is Everything

VAT is perhaps the most complex area of accounting for the Bar. Once your taxable turnover exceeds the current threshold (£90,000 as of 2024), you must register for VAT.

The “Tax Point” Confusion

For most businesses, the tax point is the date the invoice is issued. For barristers, however, there are special rules. Because of the delay in payments, many barristers use the Cash Basis for VAT, meaning they only account for VAT when the payment is actually received into their bank account.

However, if you issue a VAT invoice, that can trigger a tax point. Navigating the intersection of “Fee Notes” (which are not VAT invoices) and “VAT Invoices” (issued upon payment) is where many barristers make errors that lead to HMRC inquiries.

5. Managing Irregular Income: The 30% Rule

Because you might receive £30,000 one month and £2,000 the next, you cannot live on your “bank balance.”

The Strategy

We advise barristers to adopt a strict “Tax Reserve” policy. Every time a solicitor pays a fee note, immediately transfer 25% to 30% into a separate, high-interest savings account. This money does not belong to you; it belongs to HMRC.

By treating your gross income as “business revenue” and only your net-of-tax income as “personal salary,” you build an automatic buffer. This buffer becomes your lifeline during slow periods, such as the summer recess or during a long-running case where the brief fee hasn’t yet been triggered.

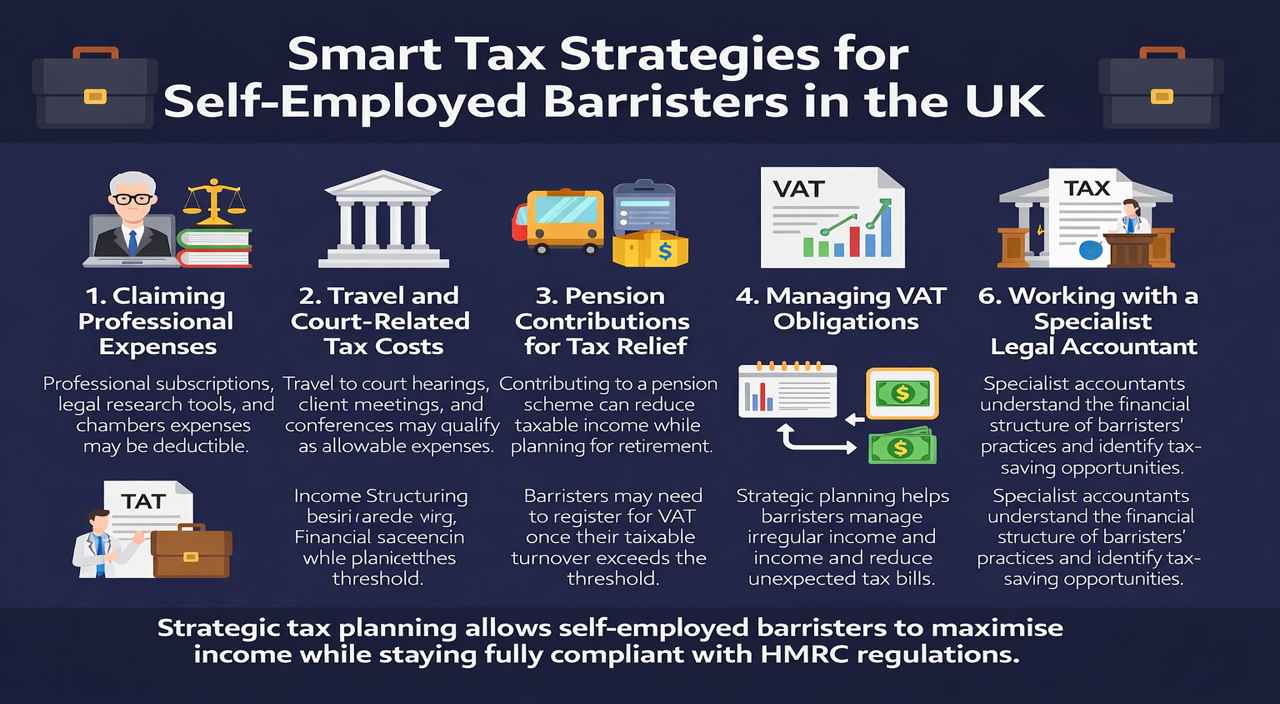

6. Allowable Tax Deductions: What Can You Actually Claim?

One of the primary benefits of being self-employed is the ability to deduct “wholly and exclusively” business expenses from your income, reducing your taxable profit.

Chambers Expenses

- Chambers Rent/Flat Rate: This is usually your largest deduction.

- Clerk Commissions: The percentage paid to your clerks for securing and managing work.

Professional Costs

- Bar Subscriptions & Practising Certificates: The mandatory costs of being at the Bar.

- Inns of Court Fees: Annual memberships and event costs.

- CPD and Training: The cost of keeping your legal knowledge up to date.

- Legal Research Tools: Subscriptions to LexisNexis, Westlaw, or specialized law reports.

Travel and Subsistence

Travel to court or to a client’s place of business is deductible. However, your daily commute to your “base” (your Chambers) is generally not deductible. If you are required to stay overnight for a case, your hotel and reasonable meal costs are allowable.

The “Wig and Gowns” Rule

HMRC allows deductions for specialized professional attire that cannot be worn as everyday clothing. This includes your wig, gown, and bands. However, standard “court suits” or shirts are generally not deductible because they provide “basic human cover” and could technically be worn outside of work even if you only ever wear them in the Robing Room.

7. Making Tax Digital (MTD): The Future of the Bar

HMRC is moving toward a fully digital tax system. Under Making Tax Digital for Income Tax Self-Assessment (MTD for ITSA), barristers with qualifying income will soon be required to:

- Keep digital records of all transactions.

- Send quarterly updates to HMRC instead of one annual return.

- Use MTD-compatible software.

For a busy barrister, the requirement to file data every three months is a significant administrative hurdle. Preparing now by transitioning from spreadsheets to cloud-based accounting software like Xero or QuickBooks is essential.

8. Financial Planning: Smoothing the Peaks and Troughs

Beyond mere tax compliance, true financial success for a barrister involves long-term wealth planning.

Pension Contributions

Contributing to a pension is one of the most tax-efficient moves a barrister can make. Contributions attract tax relief at your highest marginal rate. If you are a 45% taxpayer, a £10,000 pension contribution effectively only “costs” you £5,500, while the full £10,000 grows in a tax-sheltered environment.

Income Smoothing

Since you cannot use a Limited Company to “retain” profits, you must use other vehicles to smooth your income. This includes maximizing your ISA allowances and maintaining an emergency fund equivalent to 6 months of Chambers rent and personal expenses.

9. Why Barristers Need a Specialist Accountant

The legal world is specialized, and your accounting should be too. While many firms act as accountants for solicitors, the requirements for the Bar are distinct. A generalist accountant may not understand the specific VAT “tax point” rules for barristers or how to properly treat Chambers’ recharges.

The Mortgage Challenge

Barristers often face difficulties when applying for mortgages. Lenders see the irregular income and become hesitant. A specialist accountant understands how to present your “aged debt” and your consistent track record to lenders, proving your creditworthiness despite the fluctuating monthly deposits.

10. How Lanop Business and Tax Advisors Help the Legal Profession

At Lanop, we have built our reputation as premier accountants for solicitors and barristers alike. We understand that your time is your most valuable asset. Every hour you spend wrestling with a VAT return is an hour you aren’t billing or preparing for a trial.

Our Specialist Services for Barristers

- Bespoke Tax Planning: We look at your specific call level and practice area to optimize your tax position.

- VAT Management: We handle the complexity of the barrister VAT rules, ensuring you only pay what is owed when the cash arrives.

- Cloud Accounting Integration: We move your practice onto digital platforms, making you fully MTD-ready.

- Cash Flow Forecasting: We help you visualize your upcoming “Payments on Account” so you can invest your surplus cash with confidence.

We provide more than just a year-end service; we are your year-round financial clerks, ensuring your practice is as robust as your legal arguments.

Frequently Asked Questions

1. How does the self-employed tax system work for barristers?

As a self-employed barrister, you pay income tax on your profits (fees minus expenses) and Class 2 and Class 4 National Insurance through Self-Assessment. Tax isn’t deducted at source; you calculate what you owe and pay HMRC directly by January 31st, with a second payment on account due July 31st.

2. What expenses can barristers claim to reduce their tax bill?

You can claim chambers rent and service charges, clerks’ fees, professional subscriptions (Bar Council, Inn of Court), legal books and research subscriptions, professional indemnity insurance, wigs and gowns, travel to court, CPD courses, IT equipment, and accounting fees. Keep all receipts and only claim genuine business expenses.

3. Should I operate through a limited company or stay self-employed?

Most barristers stay self-employed because the Bar Standards Board regulates practice structures, and chambers arrangements work best this way. Limited companies can be tax-efficient at higher incomes but add complexity and may conflict with chambers’ fee-sharing. Always consult a specialist barrister accountant before considering incorporation.

4. How do I handle irregular income and manage cash flow as a barrister?

Set aside 30%–40% of every payment for tax and National Insurance in a separate account. Build an emergency fund covering 3–6 months of expenses to manage gaps between payments. Use accounting software to track outstanding fees and chase late payments systematically to maintain cash flow.

5. What are payments on account and how do they affect my tax planning?

Payments on account are advance payments toward next year’s tax, calculated as 50% of your previous year’s liability, paid in January and July. If you had a high-earning year, next year’s payments can be substantial even if income drops. Save consistently and consider applying to reduce payments if your income genuinely falls.

Final Thoughts: Securing Your Financial Future

Success at the Bar is measured by more than just the “win.” It is measured by the sustainability of your practice and the security of your future. By mastering the fundamentals of cash flow, staying ahead of digital tax changes, and claiming every legitimate deduction, you ensure that your hard work in court translates into lasting personal wealth.

Financial management shouldn’t be a source of stress. With the right systems and specialist support from Lanop Business and Tax Advisors, it can become a streamlined part of your professional life.

Ready to optimize your practice’s finances? Contact Lanop Business and Tax Advisors today for a consultation with our specialist legal accounting team. Whether you are at the start of your career or preparing for the bench, Lanop Business and Tax Advisors is here to ensure your finances are always in order.

Read more on WCCO

Cryptocurrency has become an important payment option for businesses. Many businesses prefer to accept crypto payments via a crypto payment gateway. However, there are some risks associated with online payment methods. So, a secure platform is required.

Cyberattacks are common, so one may not rely only on credentials. Additional security features are also important to make the entire payment system almost risk-free. Here, we will talk about CoinRemitter’s features that make it a risk-free platform to accept payment in crypto.

Features That Make CoinRemitter a Risk-Free Cryptocurrency Payment Gateway

Two-Factor Authentication

As discussed above, credentials alone aren’t enough to protect your Coinremitter account. You need an additional security layer, and 2FA provides that layer. After enabling this feature, the system no longer allows login without user authentication. Scanning the QR code from the screen using the Google Authenticator app becomes necessary. You will be allowed to log in only after entering a valid OTP.

Login Shield

This feature is similar to Two-Factor Authentication, with some differences. Instead of Google Authenticator, this feature uses your registered email address for authentication. After you turn on this feature, this crypto payment processor will send you an OTP to your registered email address while logging in. You will have to enter a valid OTP to authenticate yourself. This platform will not permit logins without OTP once you enable this feature. So, your login process will eventually become stronger.

Login Notification

This feature helps you know if there is any unverified user trying to access your account. Once you turn on this feature, this crypto payment gateway will send an email to your registered email address on every successful login attempt. This email will contain the browser and the device’s IP address used to log in. If you find any unidentified device, it may be an unauthorized login. Basically, this feature helps you identify unauthorized logins.

Login History

You can use this feature to detect unauthorized activities in your account. Here, you can view the list of all the login sessions. The list contains the browser, IP address, and time of the device used to access your account. Using the time and the IP address, you can detect unauthorized access. A device with an unverified IP or suspicious location may be an unauthorized access.

Active Login

This feature can help you quickly prevent unauthorized access. Here, you can view all active sessions for your account, along with the time, location, and device IP address for each session. Apart from that, there is the log-out button. You can click that button to log out of your account from a suspicious device. This feature can help you prevent unauthorized users from accessing your account.

Auto-Withdrawal

This is not a dedicated security feature, but it contributes a lot to your wallet’s security. All payments made with this crypto payment processor are deposited into your internal wallet. Auto-Withdrawal automatically transfers funds to an external wallet every thirty minutes. Business owners quickly get control over their funds, improving fund security. Also, the platform hasn’t suffered any losses due to issues such as outages, blockages, etc.

What to Do in the Case of Unauthorized Login?

To make this cryptocurrency payment gateway completely risk-free, you have to follow some steps. If any unauthorized access occurs, consider following these steps:

- Log out of your account from suspicious devices using the Active Login feature.

- Quickly disable API withdrawals from all your CoinRemitter wallets to prevent fund loss.

- Quickly set the lowest daily withdrawal limit to minimize your fund loss (in optional cases).

- Change your account and wallet passwords. Set strong passwords that don’t match your personal information, so they cannot be easily cracked.

Final Thoughts

CoinRemitter is undoubtedly one of the most secure cryptocurrency payment gateways with its KYC-free registration and other security measures. However, you can make it completely risk-free using the features mentioned above. In addition, following a few steps will further strengthen your account and wallet security. When you accept payment in crypto, such risk-free solutions are quite important to keep your personal information and funds safe.

Read more on WCCO

Finnorth stands out in the world of financial technology. It brings together tools for managing money in a smart way. This guide covers everything you need to know about Finnorth. From its basic setup to advanced options, you will find clear details here. Whether you handle personal funds or run a small business, Finnorth offers ways to make tasks easier. Read on to see how it fits into daily life and why it matters in today’s finance scene.

What Is Finnorth?

Finnorth is a fintech platform that helps people and businesses handle their finances in one place. It combines banking, budgeting, and insights into a single system. Unlike traditional banks, Finnorth uses technology to automate many steps. This means less time spent on manual work and more focus on making good choices. The platform connects to your accounts and gives a full view of your money flow. It started as a concept to fix common problems like scattered data and slow processes. Now, it serves as a tool for modern financial needs. Many users turn to Finnorth because it simplifies complex tasks without needing extra apps.

Finnorth focuses on security and ease of use. It verifies your identity during signup to keep things safe. Once set up, you can link bank accounts, credit cards, and other sources. The dashboard shows all your information at a glance. This setup helps spot trends in spending or saving. Finnorth is not just a bank; it partners with licensed institutions to offer services like transfers and loans. Its goal is to make finance accessible for everyone, from beginners to experts. By using data smartly, it provides tips tailored to your situation.

Key Features of Finnorth

Digital Banking Tools

Finnorth offers round-the-clock access to your accounts through its app or website. You can check balances, make payments, and transfer money anytime. Automated budgeting is a standout feature. It tracks your income and expenses, then suggests ways to save. For example, it can set aside money for goals like vacations or emergencies. Personalized insights come from analyzing your habits. If you spend too much on dining out, it alerts you and offers alternatives. These tools make managing funds straightforward and help avoid surprises.

AI-Powered Options

Artificial intelligence plays a big role in Finnorth. It categorizes transactions automatically, so you don’t have to sort them by hand. Fraud detection scans for unusual activity and sends alerts right away. Cash flow forecasts predict future balances based on past patterns. This helps plan for big expenses or slow income periods. Chatbots provide quick answers to questions, available all day. For businesses, AI analyzes market trends to aid decisions on loans or investments. These features add a layer of smart support, making the platform more than just a basic app.

Will You Check This Article: Damon Darling Net Worth: A Full Breakdown in 2026

Security Measures

Safety is a top priority for Finnorth. It uses strong encryption to protect your data from unauthorized access. Two-factor authentication adds an extra step when logging in. Real-time monitoring watches transactions and flags anything suspicious. Regular checks ensure compliance with rules. Users get tips on safe practices, like strong passwords. In case of issues, quick response teams handle problems. This setup builds trust, especially for those worried about online banking. Finnorth’s approach keeps your information secure while allowing easy use.

History and Growth of Finnorth

Finnorth began as an idea to improve financial management in the digital age. Around 2020, developers saw the need for a unified system amid growing online banking. Early versions focused on basic connections between accounts. Over time, it added AI and automation to stand out. Partnerships with banks allowed it to expand services like lending. By 2025, Finnorth had thousands of users, thanks to its user-friendly design. It grew through feedback, adding features based on what people wanted. Today, it operates in multiple countries, adapting to local rules. This path shows how Finnorth evolved from a simple tool to a full platform.

Growth came from addressing real problems. Many faced juggling multiple apps for banking and budgeting. Finnorth solved this by integrating everything. Investments in technology helped it scale. Events and collaborations in fintech hubs boosted its reach. For instance, ties with northern England networks inspired some features. Now, it plans expansions into new areas like sustainable finance. This history highlights Finnorth’s commitment to innovation and user needs. It continues to update based on trends, ensuring it stays relevant.

Benefits of Using Finnorth

Finnorth saves time by automating routine tasks. Instead of checking statements manually, the platform does it for you. This leads to fewer errors and better control over spending. Users often see improved savings habits through alerts and goals. For businesses, it provides clear reports for taxes or planning. Cost savings come from lower fees compared to traditional banks. Transparency is another plus; instant updates keep you informed. Overall, it reduces stress around money matters.

Security benefits give peace of mind. With advanced protection, risks like fraud drop. Personalized advice helps make smarter choices, such as cutting unnecessary costs. Accessibility means anyone with a phone can use it, broadening options for underserved groups. Small businesses gain from tools that track cash flow in real time. This can prevent shortfalls and support growth. Finnorth’s benefits extend to teams, with shared access for collaboration. In short, it makes finance more efficient and secure for all users.

Finnorth promotes better financial health. By showing patterns, it encourages positive changes. For families, it aids in planning budgets together. Freelancers benefit from invoice tracking and expense logs. The platform’s insights can lead to long-term gains, like building credit or saving for retirement. Compared to basic apps, its depth provides more value. Users report feeling more in control after switching to Finnorth.

How Finnorth Works Step by Step

To start with Finnorth, sign up on the app or site. Provide basic info and verify your identity for security. This process takes minutes. Next, link your accounts. Finnorth connects to banks and cards securely. Once linked, data flows into the dashboard. Here, you see overviews of balances and transactions.

Set up features like budgeting. Choose categories for expenses and set limits. AI helps by suggesting based on your data. For payments, select options and confirm. Automation can handle recurring bills. Insights appear as reports or alerts. Review them to adjust plans. If needed, contact support via chat. This flow makes daily use simple.

For advanced tasks, explore integrations. Connect to payroll or e-commerce tools. This pulls in more data for full views. Security runs in the background, monitoring everything. Updates happen automatically to keep things current. Finnorth’s design ensures smooth operation, even for new users.

Who Should Use Finnorth?

Finnorth suits individuals who want simple financial tracking. If you have multiple accounts, it unifies them. Families can benefit from shared views and goal setting. It helps teach kids about money through easy interfaces.

Small businesses find value in cash flow tools. Freelancers use it for invoice management and tax prep. Teams get role-based access, so everyone sees what they need. This aids collaboration without risks.

Tech-savvy users appreciate AI features for forecasts and alerts. Those new to digital banking start with basic options and grow. Finnorth targets anyone seeking efficiency in finance, from students to retirees.

Finnorth vs. Other Fintech Platforms

Finnorth differs from basic banking apps by offering deep integrations. While some apps handle transfers, Finnorth adds AI insights. Compared to platforms like Fintern, which focus on credit, Finnorth covers broader management.

Against FintechOS, Finnorth emphasizes user ease over enterprise tools. It stands out with personal touches, like custom alerts. Costs are often lower due to automation. In northern hubs like FinTech North, Finnorth draws inspiration for community focus. This makes it more accessible than London-based options.

Finnorth prioritizes security similar to others but adds education. Unlike some, it avoids high fees for premium features. Users switch for its all-in-one approach, reducing app clutter.

Related: Latest News on MyGreenBucks.net: Key Updates and Insights for 2026

Challenges and Solutions in Finnorth

One challenge is data privacy. Finnorth addresses this with strict rules and user controls. You can choose what to share. Regulatory limits vary by country, so features differ. The platform works with local laws to expand safely.

AI accuracy can be an issue. Finnorth uses human oversight for key decisions. Users can override suggestions easily. For remote areas, digital access matters. Finnorth optimizes for low-bandwidth use.

Over-reliance on tech is a risk. The platform encourages reviews of automated actions. Regular updates fix bugs and add features. These steps help overcome common hurdles.

Future Trends for Finnorth

Finnorth plans to add more AI for personalized plans. Real-time payments will speed up transfers. Open banking will enhance connections.

Sustainable finance options, like green investments, are coming. This ties into broader trends. Partnerships with tech firms will bring new tools.

Global expansion aims at more regions. Focus on user feedback will drive changes. Finnorth sees a connected ecosystem where finance fits seamlessly into life.

Why Choose Finnorth Today?

Finnorth offers a fresh way to handle money. Its tools save time and reduce worry. With strong security and smart features, it fits modern needs. Start small and scale as you go.

Many users praise its ease and insights. In a busy world, Finnorth simplifies finance. Give it a try to see the difference.

Tax and Finance Guide for Self-Employed Barristers in the UK

Quartzite Worktops: Nature’s Masterpiece for Your Kitchen

Healthcare Digital Marketing in Dubai: How Clinics Can Build Trust Online

A Complete Guide to UploadArticle.com: Your Platform for Sharing Articles Online

seo companies 2025 aelftech com – A Close Look at Services & Results

Understanding Archivebate: A Full Guide to the Webcam Archive Platform

-

Business2 months ago

Business2 months agoA Complete Guide to UploadArticle.com: Your Platform for Sharing Articles Online

-

Tech2 months ago

Tech2 months agoseo companies 2025 aelftech com – A Close Look at Services & Results

-

Lifestyle2 months ago

Lifestyle2 months agoUnderstanding Archivebate: A Full Guide to the Webcam Archive Platform

-

Tech2 months ago

Tech2 months agoUnderstanding Crackstube: A Complete Guide to the Term, Sites, and Safe Choices

-

Business2 months ago

Business2 months agoBrisbane Local SEO Companies Aelftech Com: A Complete Guide to Top Services in 2026

-

Business2 months ago

Business2 months agoThe Ultimate Guide to UploadBlog Guest Post: Everything You Need to Know

-

Finance2 months ago

Finance2 months ago5StarsStocks: A Full Guide to Better Stock Choices

-

Tech2 months ago

Tech2 months agoTop Magento Service Companies by Aelftech.com